Calls For Strategic Partnership To Optimise Dry Season Farming in Nigeria

Tag Archives: ABUJA

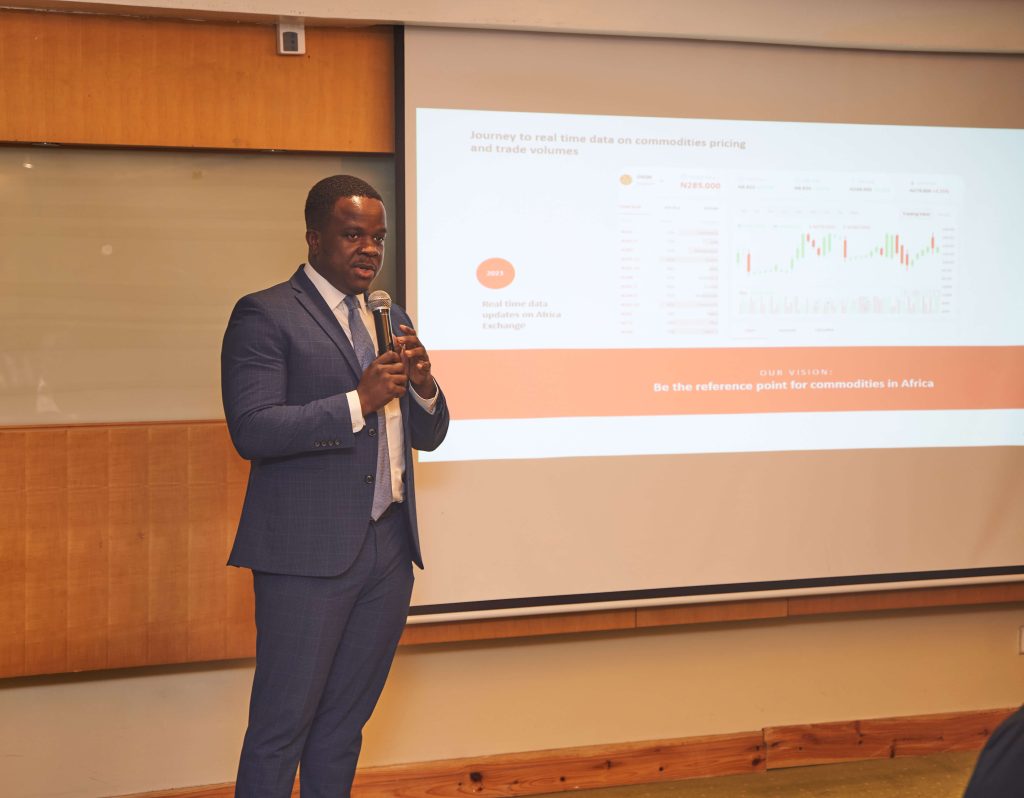

Africa’s leading commodities player, AFEX, has launched Africa Exchange, a digital platform for trading commodities.

Energy, Nigeria News

“Decarbonising Nigeria is feasible with current power technologies – and will not cost more”: Wale Yusuff, Managing Director, Wärtsilä Nigeria

Meeting last week in Abuja and Lagos for the 2023 Energy Transition Forum, Nigeria’s leading energy experts have outlined the country’s roadmap to decarbonisation, and discussed what it will take to deliver universal access to clean energy for Nigerian households and businesses.

The Carlson Rezidor Hotel Group – born in early 2012 – is one of the world’s largest and most dynamic hotel groups. The portfolio of the Carlson Rezidor Hotel Group includes more than 1,300 hotels, a global footprint spanning 80 countries, a powerful set of global brands (Radisson Blu, Radisson®, Country Inns & Suites by […]