|

When it comes to hotel development across Africa, Egypt and Marriott are the two phenomena to watch. This insight comes from this year’s African Hotel Chain Development Pipeline report, widely acknowledged as the industry’s most authoritative source, documenting and analysing the number of hotels being planned and built across the continent. The survey, conducted by Lagos-based W Hospitality Group, in association with the Africa Hospitality Investment Forum (AHIF), is based on responses from 45 global and regional (African) hotel chains, reporting on a pipeline of hotel development activity totalling around 84,400 rooms in 482 hotels, in 42 of Africa’s 54 countries. North Africa continues to dominate the pipeline, with Egypt far ahead. It alone numbers 21% of the hotels and 30% of the rooms being planned or built on the entire continent. The top ten countries represent 68% of hotels in the survey, and 74% of the rooms. |

|

|

Egypt not only leads the country table, with almost 25,000 rooms in 103 hotels, but is streaking ahead of the pack, with more than three times the number of rooms being developed in second-placed Nigeria, and four times Morocco and Ethiopia |

|

|

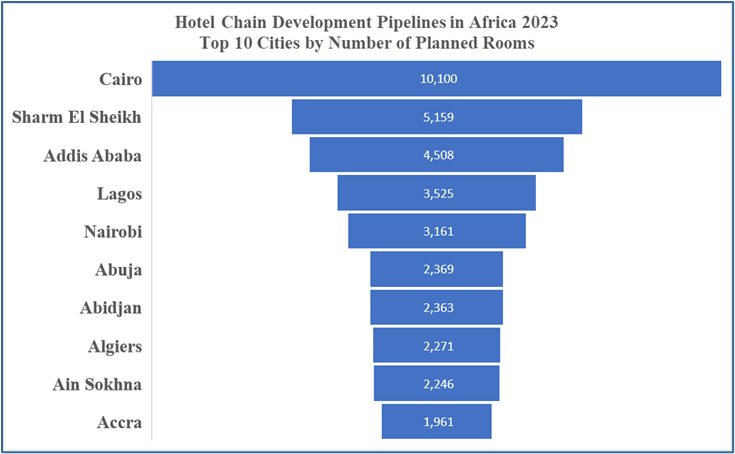

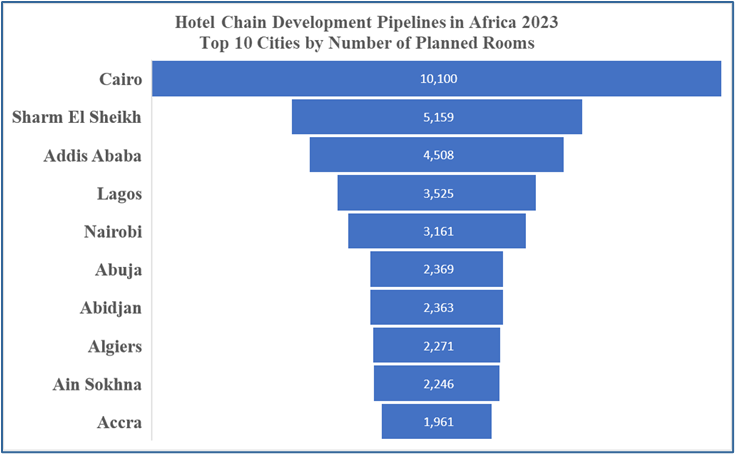

Despite its clear leadership in the absolute pipeline numbers, Egypt has the lowest percentage of rooms onsite due to its relatively “young” pipeline. Of the total 103 projects, half were signed in 2020 and later, and that’s nearly 60% of the rooms. In contrast, Morocco and Algeria have some of the highest ratios of rooms under construction on the continent. After Egypt, Nigeria has quite a low percentage onsite, and, of the 22 hotels that have started construction there, eight of them, with about half of the “onsite” rooms, have stalled (often due to a lack of funds) and the sites are closed. On a city basis, Greater Cairo has by far the largest share, 12% of the entire pipeline, followed by Sharm El Sheikh and Addis Ababa. |

|

|

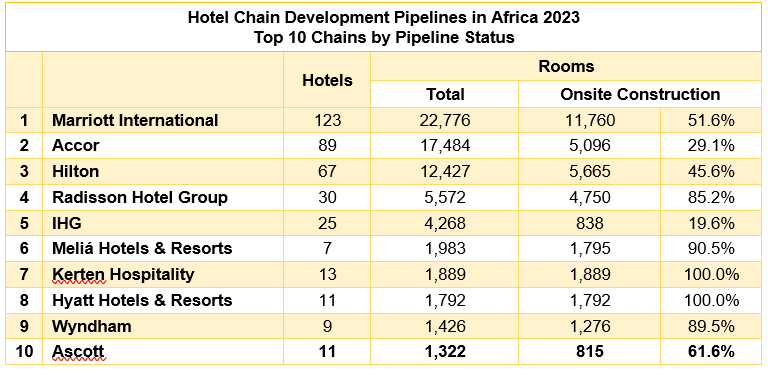

As in previous years, three international hotel chains, the USA’s Marriott International and Hilton, plus France-based Accor, top the table, with Marriott pulling firmly ahead in 2023. |

|

|

Radisson has been opening hotels at a faster pace than any other operator, with some hotels opening the same year they are signed – four in Morocco in 2021, and one in Tunisia in 2022. Marriott are projecting a massive number of openings in 2023, more than opened in total for all the chains in 2022, and Accor are projecting a catch-up with eight times their 2022 performance. Kerten Hospitality (a newcomer to the survey this year) and Hyatt Hotels & Resorts have all their pipeline on site, but Marriott International, the world’s largest hotel chain, with the largest number of rooms and the largest African development pipeline, have three times the number of rooms onsite of those two hotel chains put together. Hilton is in second place for onsite rooms, after Marriott International. |

|

|

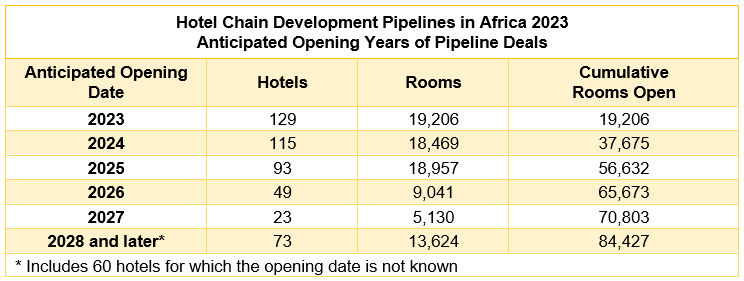

Of the total 84,427 rooms in the pipeline, over 37,500 rooms (about 45%) are expected by the hotel chains to open in 2023 and 2024. After a positive performance in 2019 (75% opened), the actualisation of hotel deals (the proportion that opened, versus what the chains expected to open) has been 30 per cent or less in the last three years – severely down for obvious reasons. The headwinds that developers have faced are mostly abating, although it can still be a challenge to open on time. |

|

|

Trevor Ward, Managing Director, W Hospitality Group said: “There are several reasons why new hotel development in Egypt is so strong, including the low value of the Egyptian pound, its unparalleled tourism assets, its proximity to major source markets and good infrastructure. One of the drivers of Marriott’s strong performance is a growing trend towards franchising in Africa, and Marriott’s relative strength in franchising with 30 brands in its portfolio. Franchising appeals to owners and investors as they retain more control of their properties; and they are now able to work with proven white-label operators in Africa to run them.” Matthew Weihs, Managing Director of The Bench, which organises the Africa Hospitality Investment Forum (AHIF), concluded: “The high expectations for 2023 and 2024 openings don’t just make a really good news story; they bode very well for AHIF, as there will be an optimistic atmosphere at the conference, which is likely to encourage participants to seek new deals and further investment opportunities.” Matthew and Trevor discuss the findings in more depth in a podcast, which can be found at: https://www.ahif.com/content- |